Here is the truth: SIP and lump sum are not competitors. They are different tools for different situations. This guide explains exactly how each one works — with real Indian examples and no jargon.

The debate around SIP vs lump sum investment India often assumes there must be a single winner. There is not — and that framing is exactly what confuses most beginners.

In this guide, you will learn how SIP and lump sum investing actually work, see real examples with Indian rupee amounts, understand the hybrid STP strategy most articles ignore, and find a simple framework to decide which approach fits your situation. If you are just starting out, read our complete guide to start investing in the Indian stock market first.

- What is SIP vs Lump Sum?

- How Each Method Works

- The Core Difference

- When Each Approach Is Used

- The Hidden Cost of Waiting for a Crash

- SIP vs Lump Sum During a Market Crash

- Salaried Investors and Bonus Income

- Hybrid Strategy — STP Explained

- The Hidden Tax Trap Inside STP

- The XIRR Illusion — Why Your SIP Looks Negative

- Why Most Articles Are Outdated on Debt Fund Tax (2023 Change)

- NRI SIP vs Lump Sum

- SIP vs Lump Sum in Nifty 50 Index Funds

- Quick Decision Quiz

- Advantages of Each Method

- Limitations of Each Method

- Key Takeaways

- Frequently Asked Questions

- Conclusion

What is SIP vs Lump Sum Investment?

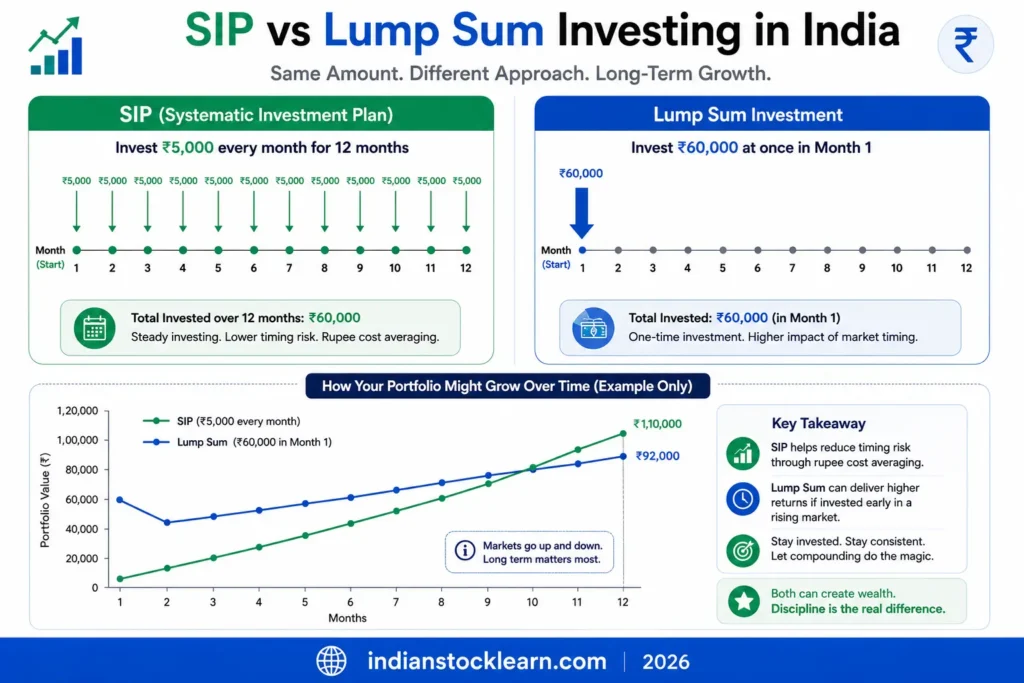

SIP (Systematic Investment Plan) and lump sum are two ways to invest money into mutual funds or index funds. The difference is not about which fund you choose — it is about when and how money enters the market.

| Method | What You Do | Simple Example |

|---|---|---|

| SIP | Invest a fixed amount at regular intervals — usually monthly | ₹5,000 every month into a Nifty 50 Index Fund on the 5th |

| Lump Sum | Invest a larger amount in a single transaction | ₹60,000 invested once into the same fund |

Both approaches can lead to wealth creation over time. The difference is that SIP focuses on consistency and averaging, while lump sum focuses on immediate market exposure. Understanding the Nifty 50 index helps you understand what both methods are actually investing in.

How SIP and Lump Sum Investing Work

How SIP WorksWith a SIP, money is automatically invested on a fixed schedule. No manual action is needed after the first setup. Here is the key mechanism that makes SIP useful during volatile markets:

- When markets fall, your fixed ₹5,000 buys more units

- When markets rise, the same ₹5,000 buys fewer units

- Over time, this creates a natural averaging of your purchase price — known as rupee-cost averaging

This averaging effect is why SIP is often described as a lower-anxiety approach to investing for salaried individuals.

How Lump Sum Investing Works

A lump sum investment places the entire amount into the market at once. The entire investment is exposed to market performance from day one.

The Core Difference: Market Timing Exposure

The biggest difference between SIP vs lump sum investment in India is how much market timing risk you take on. Think of it like filling a fuel tank:

A lump sum investor fills the entire tank at one petrol price. A SIP investor adds fuel gradually — sometimes at ₹95/litre, sometimes at ₹110/litre — and pays an average price across all fills.

| Factor | SIP | Lump Sum |

|---|---|---|

| Investment style | Regular, automatic | One-time transaction |

| Market timing risk | Lower — spread across time | Higher — all at one point |

| Capital required upfront | Small monthly amount | Larger lump amount needed immediately |

| Behavioural ease | Often easier — set and forget | Can be emotionally difficult during volatility |

| Best scenario | Regular monthly income | One-time bonus or windfall |

| Worst scenario | Missing payments breaks consistency | Market drops sharply right after investment |

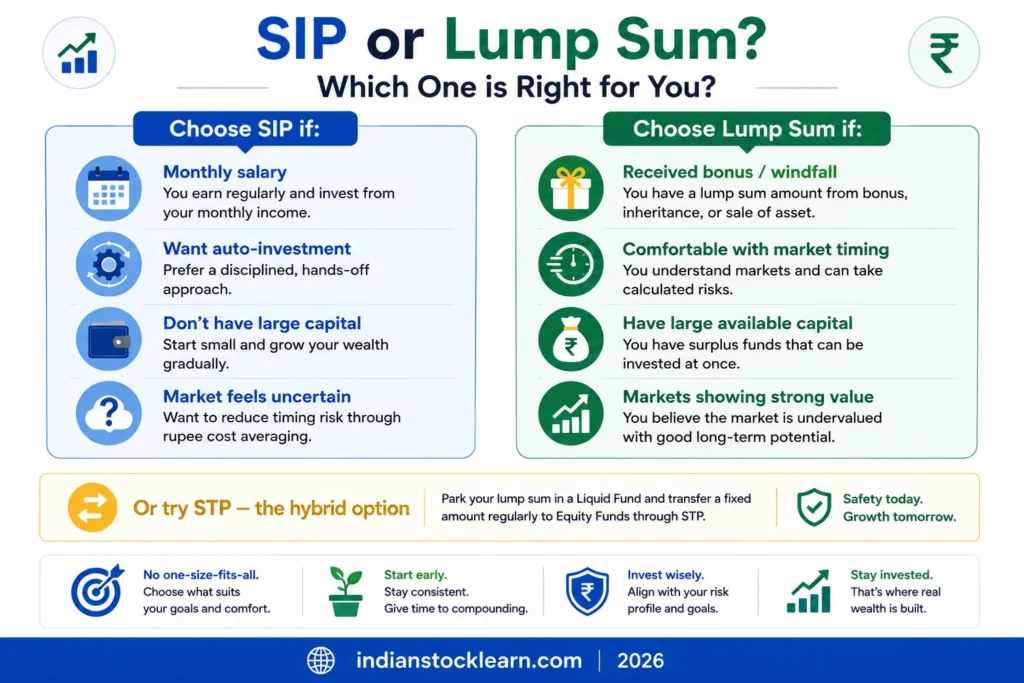

When Each Approach Is Commonly Used

🔵 SIP is commonly used when:

- You earn a regular monthly salary

- You want investing to feel automatic

- You do not have a large amount available immediately

- You prefer gradual market participation

- Market conditions feel uncertain or volatile

- You are a first-time investor building confidence

🟢 Lump sum is commonly used when:

- You receive a year-end bonus

- You sell a property or asset

- You receive an inheritance

- You have a large cash reserve sitting idle

- Markets appear to offer strong value (low PE ratio)

- You are comfortable with short-term price fluctuations

The Hidden Cost of Waiting for a Crash

One of the most common decisions Indian investors make after receiving a large bonus is: “I’ll wait for a market crash before investing the lump sum.” This feels rational. It is rarely as profitable as it sounds.

The “Cash Drag” Problem

Every month your money sits in a savings account earning 3.5% interest, the market may be returning 12–15% annually. Here is what that costs you in real rupees:

| Scenario | Investor A — Waits for Crash | Investor B — Invests Today |

|---|---|---|

| Starting amount | ₹5,00,000 in savings account | ₹5,00,000 invested in Nifty 50 fund |

| Year 1 | Earns ₹17,500 (3.5% savings rate) | Market rises 14% → portfolio ₹5,70,000 |

| Year 2 | Still waiting. Market rises another 20%. | Portfolio grows to ₹6,84,000 |

| “Crash” arrives | Market drops 25% — now at same level as Day 1 | Portfolio drops to ₹5,13,000 — still ahead of savings account |

| Cost of waiting | Missed ₹13,000+ in dividends + 2 years of growth | Temporary paper loss, but recovered faster |

The “Rule of 3” — A Practical Compromise

If you cannot bring yourself to invest a large lump sum all at once, use the Rule of 3: split the amount into three equal parts and invest one part each month for three consecutive months. This is not SIP — it is a manually controlled phased entry that limits timing regret without indefinitely delaying the investment.

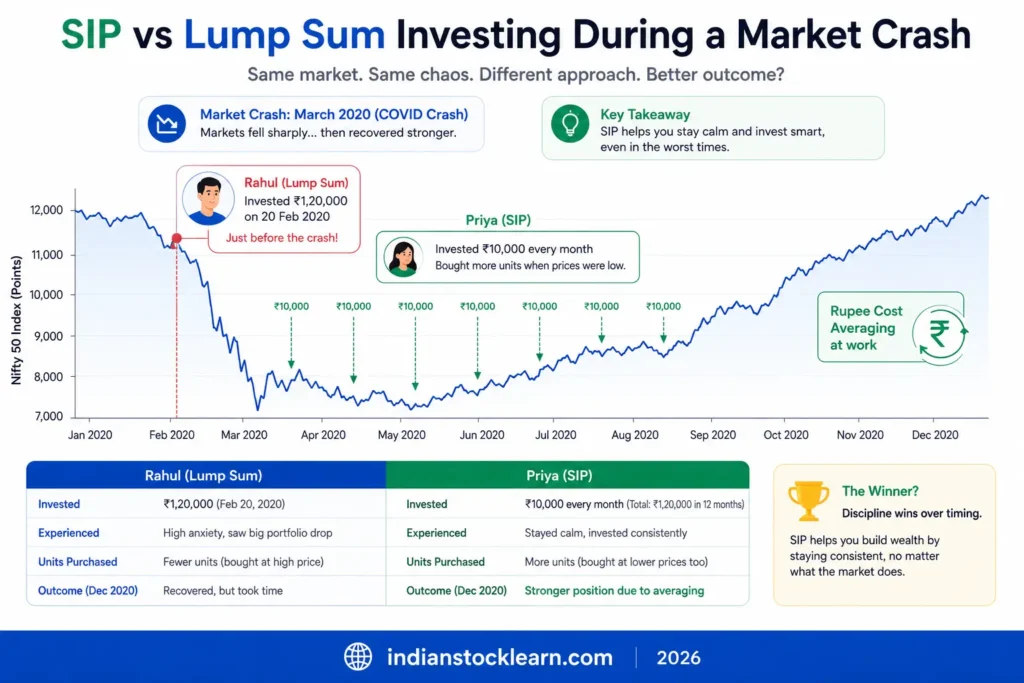

SIP vs Lump Sum During a Market Crash

This is where investor psychology becomes the real differentiator. During the COVID-19 market crash in March 2020, the Nifty 50 index fell sharply within weeks. Two hypothetical investors illustrate the difference:

| Method | Lump Sum |

| Amount | ₹1,20,000 at once |

| Timing | Invested just before the crash |

| Experience | Portfolio dropped immediately — waited for recovery |

| Method | SIP |

| Amount | ₹10,000 per month |

| Timing | Continued investing through the crash |

| Experience | Bought more units at lower prices during the dip |

As markets recovered, Priya had accumulated units at multiple lower price levels during the correction. Rahul’s full investment had to wait for the market to recover before showing gains. This illustrates why many first-time investors find SIP emotionally easier during volatile periods — but it is important to note that neither outcome is guaranteed in advance. If markets had risen immediately after Rahul’s investment, his lump sum would have outperformed Priya’s SIP by a significant margin.

SIP vs Lump Sum for Salaried Investors and Bonus Income

This is the most practical comparison for Indian investors — because most beginners face one of these two situations:

Situation 1: Monthly Salary

A salaried employee earning ₹60,000/month naturally suits SIP. The investment flows alongside their income — ₹5,000 invested each month matches how money actually arrives. There is no pressure to time the market or identify the “right” entry point. To learn how to set this up, read our guide on how to buy your first stock in India.

Situation 2: Year-End Bonus of ₹50,000

A bonus creates a different decision. Three common approaches:

| Approach | What You Do | Trade-Off |

|---|---|---|

| Invest all at once | ₹50,000 into a Nifty 50 fund on one day | Full market exposure immediately. Higher timing risk. |

| Spread into future SIPs | Add ₹50,000 to monthly SIP mandate | Gradual exposure. Takes time for full deployment. |

| STP (Hybrid) | ₹50,000 into a liquid fund → ₹5,000/month transferred to equity | Best of both: money works from day one and enters equity gradually. |

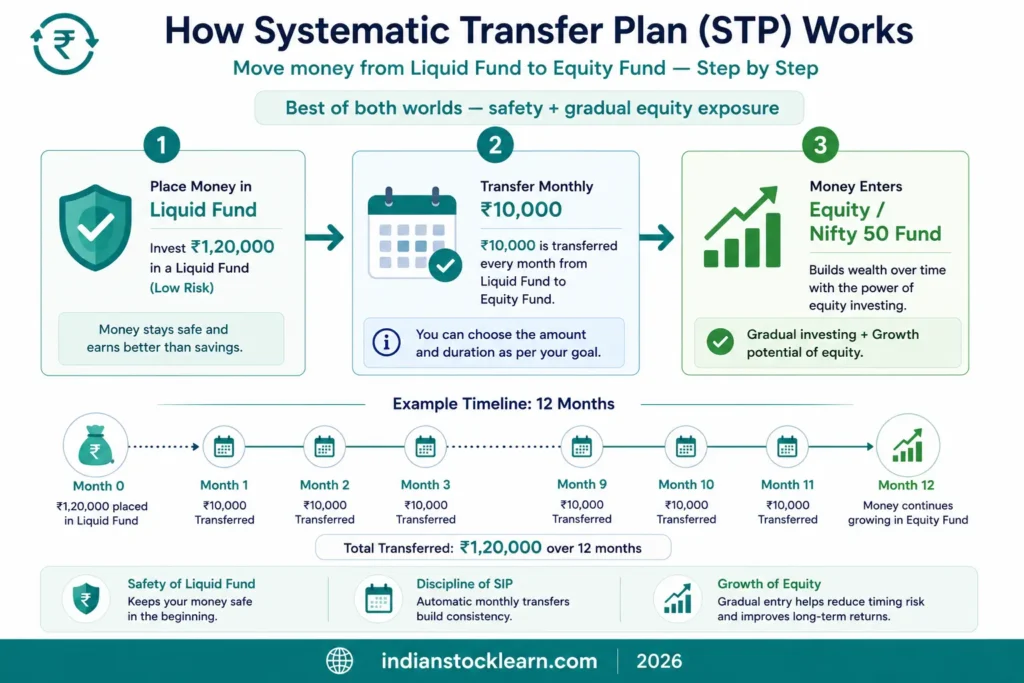

Hybrid Strategy — Using SIP and Lump Sum Together (STP)

Most beginner articles on SIP vs lump sum mutual fund investment India present this as a binary choice. It is not. A third option exists that most guides skip entirely: the Systematic Transfer Plan (STP).

| Step | What Happens | Why It Helps |

|---|---|---|

| 1 | ₹1,20,000 invested into a Liquid Fund | Capital earns ~6–7% returns immediately rather than sitting idle |

| 2 | ₹10,000 transferred monthly into a Nifty 50 fund (auto) | Gradual equity entry — same averaging benefit as SIP |

| 3 | Transfer continues for 12 months | Full equity deployment without lump sum timing risk |

An STP is often used by experienced mutual fund investors precisely because it provides gradual market entry while still putting all available cash to work from day one. It avoids both the “my money is doing nothing in a savings account” problem and the “I timed the market badly” problem.

The Hidden Tax Trap Inside STP — What Most Articles Skip

STP is genuinely useful — but most beginner articles recommend it without mentioning the tax mechanics that come with it. Before you set up an STP, understand what is actually happening under the hood.

| STP Mechanic | What Actually Happens | Tax Impact |

|---|---|---|

| Monthly transfer | Liquid fund units are sold; equity units are bought | Gains on sold liquid fund units = Short-Term Capital Gains (STCG) taxed at your income slab rate |

| 12-month STP | 12 separate sell events at the liquid fund | 12 capital gains entries in your annual tax statement (Form 26AS / AIS) |

| 7-day exit load | Many liquid funds charge exit load if units sold within 7 days of purchase | Setting up a daily or weekly STP immediately after lump sum investment triggers this charge |

| FIFO rule | AMC sells the oldest units first when calculating gains | Tax calculation complexity increases with each transfer |

The XIRR Illusion — Why Your SIP Looks Negative in Year One

If you have ever checked your SIP after 6–12 months and panicked because it showed a negative return, this section is for you. The number your app displays is not lying — but it is also not telling the full story.

| What You See (Myth) | What’s Actually Happening (Reality) |

|---|---|

| “My SIP shows 15% XIRR — that means I made 15% on my money” | XIRR is an annualised rate. A 1-year SIP showing 15% XIRR translates to roughly 7.5% absolute gain — because your last installment has only been invested for 1 month, not a full year. |

| “My SIP shows -8% after a market dip — SIPs don’t work” | During the first 2–3 years, even a normal 10% market correction can push XIRR deep into negative territory. This is a mathematical side-effect of recent installments, not proof that SIP has failed. |

| “Rupee-cost averaging means I can’t lose money” | Averaging only lowers your average purchase price — it does not protect your final portfolio value from a market decline. If the index itself falls and stays flat for years, the SIP will not magically generate positive returns. |

| “If my SIP is negative, I should stop it” | Stopping a SIP during a dip is the opposite of what rupee-cost averaging is designed for — you would be exiting exactly when units are cheapest. |

Understanding this prevents the single most common SIP mistake: stopping the investment right when it is working hardest — during a dip, when each instalment is buying more units at a lower price.

Why Most SIP vs Lump Sum Articles Are Outdated on Debt Funds

If you are comparing SIP vs lump sum for the debt portion of your portfolio — not just equity — there is a rule change from 2023 that most beginner articles still get wrong. Many guides online were written before this change and never updated.

| When You Invested | Tax Treatment | Effective Impact |

|---|---|---|

| Before April 1, 2023 | LTCG at 12.5% without indexation (if held 24+ months and sold after July 23, 2024) | Rules changed twice — older investments got a reduced rate but lost indexation |

| On or after April 1, 2023 | Taxed entirely at your income tax slab rate — no LTCG benefit at all | Up to 30% tax for higher income slabs, same as a fixed deposit |

This matters directly for your SIP vs lump sum decision: if you are using a debt fund or liquid fund as a parking space (for example, the liquid fund leg of an STP), any gains generated there — even for a few months — are taxed at your slab rate. There is no longer a tax advantage to holding a debt fund for 3 years versus 3 months. The holding-period strategy that used to make debt funds tax-efficient no longer applies.

NRI SIP vs Lump Sum Mutual Fund Investment

Non-Resident Indians often face a different version of this decision. They may have access to larger overseas savings but cannot actively monitor Indian markets from abroad. Both approaches work for NRIs, with some additional considerations:

| Factor | NRI SIP | NRI Lump Sum |

|---|---|---|

| Account type | NRE or NRO account | Usually NRE account for repatriation |

| Monitoring needed | Minimal — automated monthly | More attention at entry point |

| Best for | NRIs with regular foreign income | NRIs transferring a large saved amount |

| Regulations | FEMA, KYC, fund eligibility | Same FEMA rules apply |

Before investing, NRIs should verify KYC requirements, tax treatment under DTAA (Double Taxation Avoidance Agreement), and which specific funds allow NRI investment. The choice between SIP vs lump sum investment India remains linked to cash flow, risk tolerance, and personal investment behaviour — regardless of residency status.

SIP vs Lump Sum in Nifty 50 Index Funds

The Nifty 50 index is a straightforward example because it tracks India’s 50 largest listed companies — Reliance Industries, TCS, HDFC Bank, Infosys, ICICI Bank, and others. Both SIP and lump sum investors are buying ownership in these same businesses. The difference is purely about timing and execution.

| Total investment | ₹1,20,000 |

| Method | ₹10,000 per month × 12 |

| Units purchased | At 12 different NAV levels |

| Market timing | Automatically averaged out |

| Total investment | ₹1,20,000 |

| Method | All at once — Month 1 |

| Units purchased | At 1 single NAV level |

| Market timing | Entirely dependent on entry point |

Over a rising market period, Investor B often ends up with more units (because all capital was exposed earlier). Over a volatile or declining-then-recovering period, Investor A often benefits from rupee-cost averaging. The underlying businesses — Reliance, TCS, HDFC Bank — are identical in both portfolios. The investment method affects timing, not the quality of what is owned. Understanding the PE ratio of the index helps assess whether current valuations favour lump sum entry.

Quick Decision Quiz: Which Approach Fits Your Situation?

- Do you receive regular monthly income (salary or freelance)?

- Do you currently have a large investable amount sitting unused?

- Would a 15% market decline in the first month make you want to sell?

- Can you actively monitor and research markets regularly?

This is an educational framework, not financial advice.

| Your answers suggest | Approach to consider | Why |

|---|---|---|

| Mostly regular income, no large capital | SIP | Matches your natural cash flow. Discipline builds automatically. |

| Large available capital, comfortable with volatility | Lump Sum | All capital works immediately. Markets historically reward patience. |

| Large capital but nervous about timing | STP | Money works from day one. Equity entry is gradual. Best of both. |

| Monthly income + occasional bonus | SIP + occasional Lump Sum | Many experienced Indian investors use both simultaneously. |

Advantages of SIP and Lump Sum Investing

✅ SIP Advantages

- Builds long-term investing discipline

- Lower market timing pressure

- Ideal for regular monthly income

- Easy to automate — set and forget

- Rupee-cost averaging benefits during volatility

- Psychologically easier for beginners

✅ Lump Sum Advantages

- All capital starts working immediately

- Simple one-time transaction

- Ideal for bonus, inheritance, or asset-sale proceeds

- No need for recurring contributions

- Can outperform SIP in consistently rising markets

- Full exposure from day one in strong bull markets

Limitations of SIP and Lump Sum Investing

| Method | Limitation | When It Hurts Most |

|---|---|---|

| SIP | Requires long-term consistency — missing payments breaks the averaging benefit | During job loss or irregular income periods |

| SIP | May lag during strong, sustained upward market rallies | Bull markets where early lump sum entry would have been better |

| SIP | Takes time to build a meaningful corpus | When you have available capital but spread it too gradually |

| Lump Sum | Higher market timing risk — all capital enters at one price | When invested just before a market correction |

| Lump Sum | Can create emotional stress during early portfolio declines | First-time investors who panic-sell at a loss |

| Lump Sum | Requires larger upfront capital — not suitable for everyone | Investors without a large investable amount readily available |

Key Takeaways

- SIP invests gradually over time. Lump sum invests in a single transaction. Both are legitimate.

- Market timing matters more with lump sum — all capital enters at one point.

- SIP benefits from rupee-cost averaging — buying more units when prices fall.

- STP (Systematic Transfer Plan) combines both approaches — worth understanding if you have a large amount to invest.

- Neither method automatically outperforms in every market environment.

- The better approach often depends on available capital, cash flow, and personal comfort with risk.

- Many experienced Indian investors use both simultaneously — SIP for monthly income, lump sum for bonus or windfall amounts.

- The fund you choose matters more than the method you use to invest in it — understand PE ratio, dividends, and where your fund trades before investing.

Frequently Asked Questions

Is SIP always better than lump sum investment in India?

Should I invest lump sum or SIP after getting a bonus in India?

Can I do both SIP and lump sum investing at the same time?

Which is better — SIP or lump sum — when the market is at an all-time high?

Is lump sum investment riskier than SIP in India?

What is rupee-cost averaging and how does it work with SIP?

Should I do SIP or lump sum with ₹5 lakh?

Conclusion

The debate around SIP vs lump sum investment India often assumes there must be a single winner. In reality, both approaches exist because investors face genuinely different situations — and both have produced wealth for disciplined long-term investors in Indian markets.

A salaried professional investing ₹5,000 every month has a different situation than someone who just received a ₹3 lakh bonus. A first-time investor nervous about market crashes has different needs than someone who watched markets for five years before investing. The right approach matches your actual cash flow, your risk tolerance, and — most importantly — the approach you will actually stick with long enough for compounding to work.

If you are just starting out, a simple Nifty 50 index fund SIP is one of the most straightforward ways to begin. Learn more in our guide on how to start investing in the Indian stock market.