This guide is for Rohan. And for anyone who has hesitated at that exact screen.

India added over 4 crore new demat accounts in the past two years. Most delays — and most rejections — happen not because of complex regulations, but because of simple, avoidable document mistakes.

In this complete guide on documents required for demat account India, you will learn exactly which documents are mandatory, which are optional, what happens at each step of the process, and how to avoid the 6 most common rejection reasons. To understand why you even need a demat account before investing, read our guide on what the stock market is first.

- Documents Required — Full Overview

- How the Account Opening Process Works

- Quick Checklist Table

- PAN Card — The Most Important Document

- Aadhaar Card and e-KYC

- Bank Account Proof

- Address Proof Requirements

- Do You Need Income Proof?

- Documents for Students

- Documents for NRIs

- 6 Common Rejection Reasons

- The Penny Drop Bank Verification Trap

- KRA Holds — Hidden Rejection Layer

- Myth vs Reality: What Brokers Actually Check

- Why Brokers Ask for These Documents

- Prepared vs Unprepared — Real Difference

- Advantages of Digital KYC

- Key Takeaways

- Frequently Asked Questions

- Conclusion

Documents Required to Invest in Stock Market India — Full Overview

When you open a demat account and trading account in India, your broker must verify your identity, address, and bank details as per SEBI’s KYC (Know Your Customer) regulations. This is not a broker-specific rule — every SEBI-registered broker in India follows the same mandatory framework.

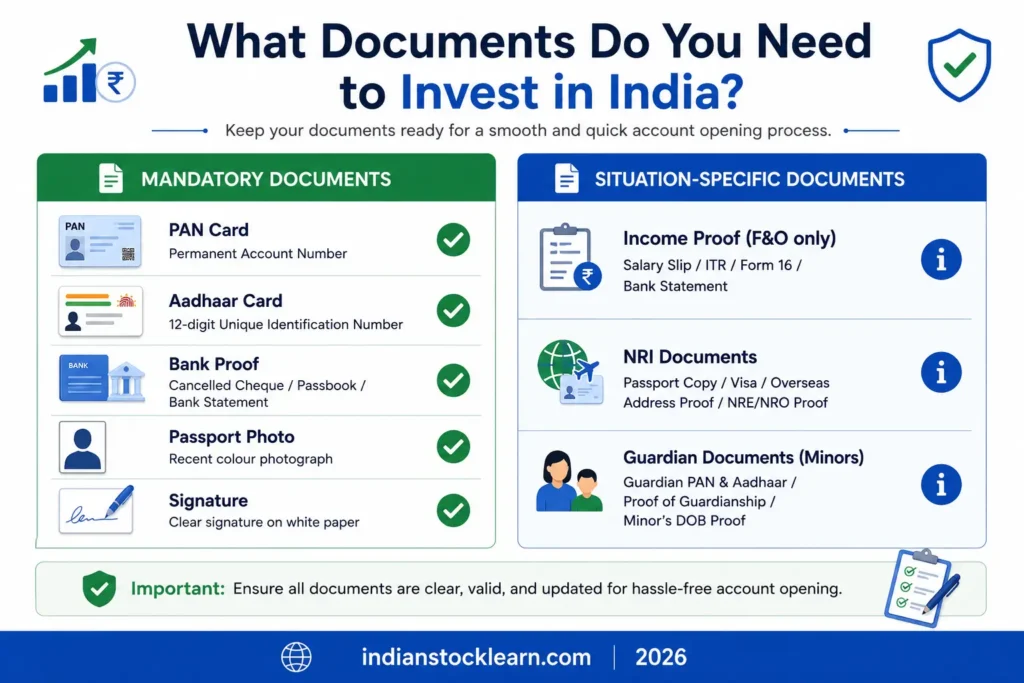

The documents needed to invest in stock market India fall into two clear categories:

| Category | Documents | Who Needs This |

|---|---|---|

| Always required | PAN Card, Aadhaar Card, Bank Proof, Passport Photo, Signature | Every investor — resident Indian |

| Situation-specific | Income Proof | Only for F&O (derivatives) trading |

| NRI-specific | Passport, Overseas Address Proof, NRE/NRO account docs | Non-Resident Indians only |

| Minor accounts | Birth certificate, Guardian’s PAN + address proof | Investors under 18 only |

Think of the demat account process like opening a bank account — the bank wants to know who you are, where you live, and how to reach you financially. Brokers follow the same logic, just with a focus on your stock market identity.

How the Account Opening Process Works

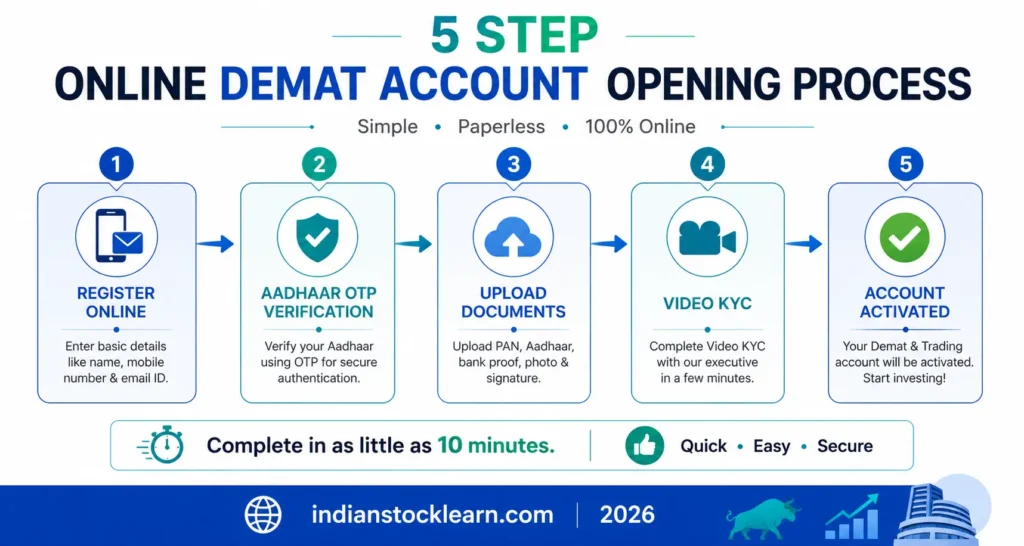

Most Indian brokers (Groww, Zerodha, Upstox, Angel One) offer a 100% online account opening process. Understanding the steps helps you know exactly which document is needed at which point.

Enter mobile number, email, and PAN number in the broker app. This is where your PAN is first verified against NSDL/CDSL records.

Your Aadhaar-linked mobile number receives an OTP. This confirms your identity and address digitally — no physical form needed.

Upload PAN card, bank proof, and signature. Some brokers also accept DigiLocker documents — faster and less likely to be rejected for quality issues.

A 2–3 minute live video call where you show your PAN card to the camera. Have good lighting and your documents physically ready.

After approval, you receive your demat account number (DP ID) and trading credentials via email. Shares can be purchased immediately after funding.

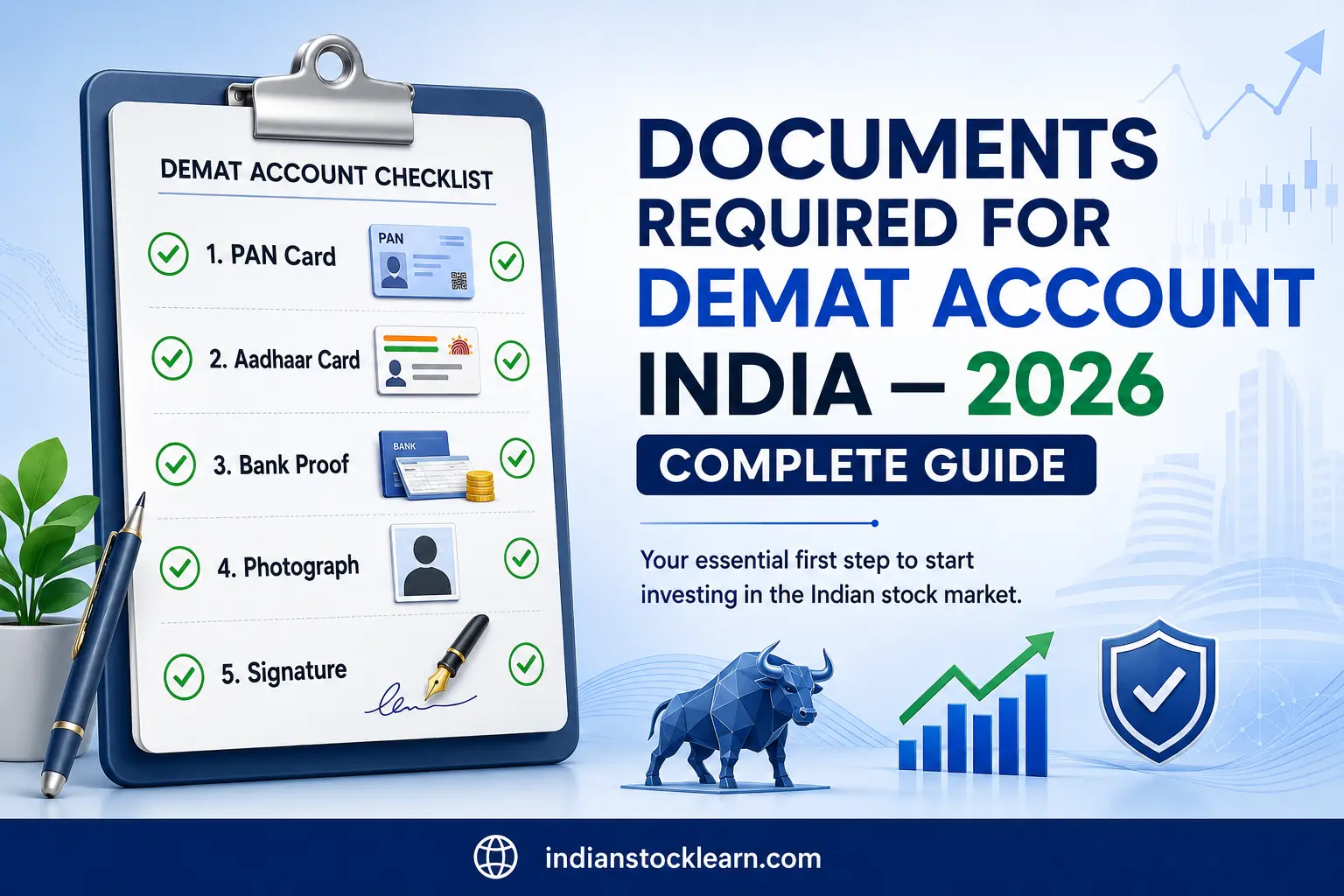

Quick Checklist: Documents Required for Demat Account India

Before opening your application, keep these documents ready in digital format (clear photos or PDFs):

| Document | Mandatory? | Purpose | Accepted Alternatives |

|---|---|---|---|

| PAN Card | Yes | Tax identity — mandatory by SEBI | No alternative accepted |

| Aadhaar Card | Yes (usually) | Identity + address + e-KYC | Passport / Voter ID / Driving Licence |

| Bank Proof | Yes | Link trading account to bank | Cancelled cheque / bank statement / passbook |

| Passport Photo | Yes | Visual identity verification | Recent clear photo (digital accepted) |

| Signature | Yes | Legal documentation | Digital signature (e-sign via Aadhaar OTP) |

| Income Proof | F&O only | Risk eligibility for derivatives | ITR / Salary slips / Bank statement / Form 16 |

| NRI Documents | NRIs only | Cross-border compliance | Passport + overseas address + NRE/NRO account |

PAN Card — The Most Important Document

Your Permanent Account Number (PAN) is the single most important document in the Indian stock market system. Every transaction you make — every share you buy or sell — is linked to your PAN for tax tracking purposes.

The National Stock Exchange (NSE) and SEBI both mandate PAN as a mandatory KYC requirement for all demat and trading accounts. There is no alternative or exception for resident Indian investors.

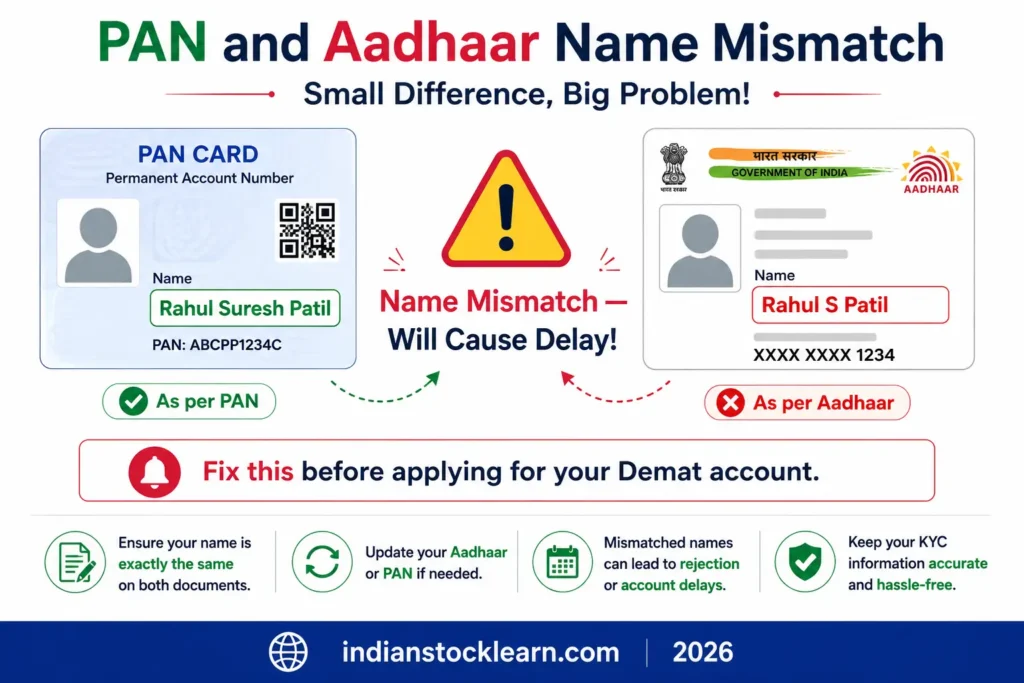

What Must Match on Your PAN

| Detail | Must Match With | If Mismatch |

|---|---|---|

| Full name | Aadhaar, bank records | Application held — additional proof requested |

| Date of birth | Aadhaar | Immediate rejection in most broker systems |

| Father’s name | Broker KYC records | Manual verification required — adds 2–5 days |

Aadhaar Card and e-KYC — The Fast Track to Account Opening

Aadhaar has transformed the demat account opening process. What once took 2 weeks of paperwork and branch visits now takes 10 minutes on a smartphone — thanks to Aadhaar-based e-KYC.

What is e-KYC?

Electronic Know Your Customer (e-KYC) is a digital verification process where your Aadhaar details (identity, address, biometrics) are verified instantly via OTP. Instead of submitting physical forms, you approve the verification through a one-time password sent to your Aadhaar-linked mobile number.

| Method | Time Taken | Documents Needed at Branch | Best For |

|---|---|---|---|

| Aadhaar e-KYC (OTP) | 10–30 minutes | None — fully digital | Most beginners |

| DigiLocker Verification | 15–45 minutes | None — documents fetched digitally | Those with DigiLocker set up |

| Video KYC | Same day | Physical PAN ready for camera | Required by some brokers |

| Offline / Paper KYC | 5–10 business days | Physical copies + in-person visit | Those without Aadhaar OTP access |

What if PAN and Aadhaar Addresses Are Different?

This is extremely common — many people update their address on one document but not the other. Your broker may request additional address proof in this case. The simplest solution: use Aadhaar as your primary address proof (since e-KYC fetches it directly) and separately submit one more address document that matches your current residence.

Bank Account Proof — What Exactly Counts

Your trading account must be linked to a bank account. Every time you buy shares, money is debited from this bank account. Every time you sell, proceeds are credited back. Without a verified bank link, the account cannot be activated.

| Bank Proof Type | Accepted? | What It Must Show |

|---|---|---|

| Cancelled cheque | Yes | Account number + IFSC code + name pre-printed |

| Bank statement (last 3 months) | Yes | Name, account number, IFSC, bank logo |

| Passbook first page | Yes | Name, account number, IFSC, branch details |

| Bank verification certificate | Yes | Issued by bank, signed by manager |

| UPI screenshot only | No | Not accepted — does not show IFSC |

Address Proof Requirements

Address verification confirms where you currently reside. Brokers use this for regulatory compliance and to send account-related communications.

| Document | Accepted as Address Proof? | Notes |

|---|---|---|

| Aadhaar Card | Yes — preferred | Accepted as both identity AND address — one document does both |

| Passport | Yes | Must be valid (not expired) |

| Voter ID | Yes | Address on card must match current residence |

| Driving Licence | Yes | Must be valid and not expired |

| Utility Bill | Yes | Must be less than 3 months old |

| Bank Statement | Yes | Recent — same document used for bank proof |

| Rent Agreement | Some brokers | Check with your specific broker |

The simplest approach for most beginners: use Aadhaar for both identity and address proof. It handles both requirements in one document and is instantly verifiable via e-KYC. To understand how the regulatory body behind all these requirements works, read our guide on what SEBI is and how it protects investors.

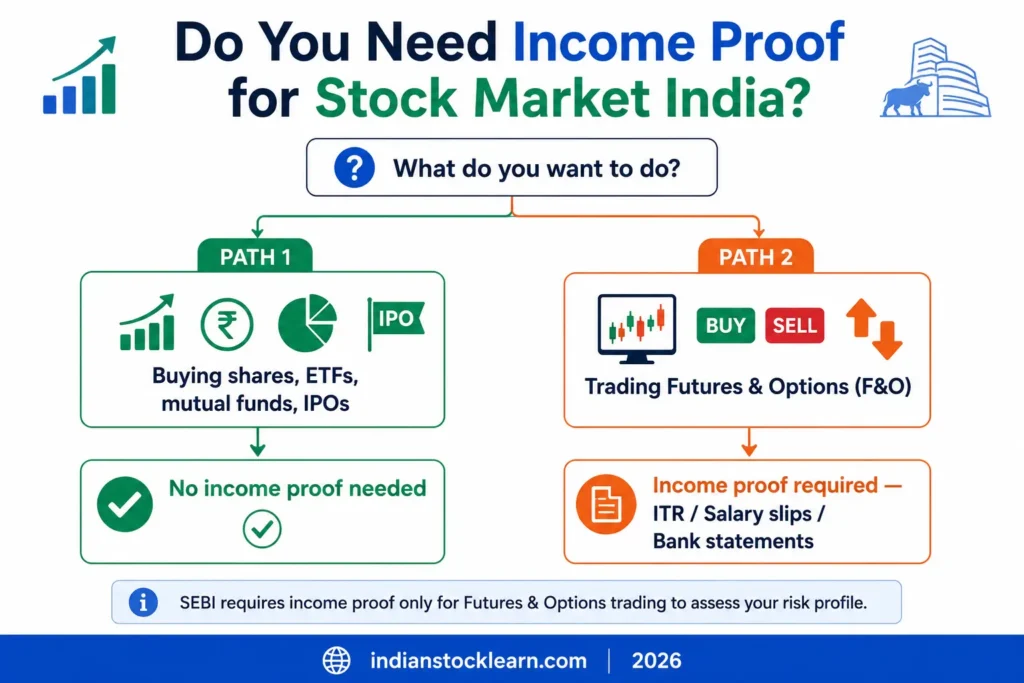

Do You Need Income Proof to Invest in Stock Market India?

This is the most common source of confusion among beginners — and the most common reason people think the process is more complicated than it actually is.

| What You Want to Do | Income Proof Needed? | Why |

|---|---|---|

| Buy shares (delivery/CNC) | No | Standard equity — no special eligibility required |

| Invest in mutual funds / ETFs | No | No leverage involved |

| Apply for IPOs | No | Standard application process |

| Intraday trading (MIS) | No | Not required for cash segment |

| Futures & Options (F&O) | Yes | Higher risk — SEBI mandates income eligibility check |

| Commodity derivatives | Yes | Same as F&O — risk-based requirement |

Documents Required for Students

Many college students want to start learning about investing — and the good news is that there is no minimum income or age restriction (for those 18+) to open a basic demat account for equity investing.

| Document | Required for Students? | Note |

|---|---|---|

| PAN Card | Yes | Apply at nearest PAN centre or online via NSDL/UTITSL if you don’t have one |

| Aadhaar Card | Yes | Mobile number must be linked |

| Bank Account (savings) | Yes | Student savings accounts (zero-balance) are accepted |

| Income Proof | No | Not required for basic equity investing |

| College ID / Proof of study | No | Not required — age-based eligibility only |

Students who want to buy their first stock in India can start with as little as ₹200–₹500 — the price of a single ETF unit. Starting early helps build familiarity with how companies like Reliance, TCS, or Infosys actually perform over time.

Documents Required for NRIs to Invest in Indian Stock Market

Non-Resident Indians can invest in Indian stocks, but the documentation process involves additional regulatory requirements beyond standard KYC.

| Document | Required? | Purpose |

|---|---|---|

| PAN Card | Yes | Mandatory — same as resident Indians |

| Passport (valid) | Yes | Primary identity document for NRIs |

| Overseas address proof | Yes | Utility bill / bank statement from country of residence |

| NRE or NRO bank account | Yes | All NRI investments must flow through designated accounts |

| FEMA declaration | Yes | Foreign Exchange Management Act compliance |

| Visa copy | Some brokers | Confirms NRI status |

NRI accounts may take longer to activate (typically 5–10 business days) due to the additional regulatory checks involved. For a complete understanding of what you can invest in via the IPO route, check our guide specifically for NRI investors.

6 Common Rejection Reasons — And How to Fix Them

Most account rejections are preventable. Here are the 6 most common causes and the exact fix for each:

Even “Rahul S Patil” vs “Rahul Suresh Patil” can trigger a hold. Fix: update Aadhaar name to match PAN exactly (free at Aadhaar centre).

Broker AI scanners reject low-quality images. Fix: photograph documents in natural light, all 4 corners visible, no shadows, minimum 200 KB file size.

Mistyped bank IFSC causes payment linking failure. Fix: cross-check IFSC on your bank’s official website or on the cheque leaf — do not type from memory.

Utility bills older than 3 months are rejected. Fix: use Aadhaar (never expires) as address proof, or download a fresh bank statement from your app.

Signature on application doesn’t match uploaded signature sample. Fix: use the same pen style and keep it consistent — brokers compare the two.

Low light, bad audio, or PAN card not clearly visible causes rescheduling. Fix: sit near a window, hold PAN steady facing the camera, speak clearly when asked.

The Penny Drop Trap: Why Your Bank Verification Actually Fails

Most beginners assume bank verification means a human checks their cancelled cheque. It does not. Brokers use an automated API process called Penny Drop verification — the system deposits ₹1 into your account and fetches the registered account holder name from the bank. That fetched name is then matched against your PAN card name by software, not a person.

This is why bank verification can fail even when your documents are perfectly correct.

Fix: Upload a stamped bank statement or a pre-printed cancelled cheque leaf (your name printed on it, not handwritten). This triggers a 48-hour manual review that bypasses the API match.

Scenario 2 — Joint account trap: If you are the second holder on a joint account, the Penny Drop fetches the first holder’s name — which will never match your PAN. The application is rejected immediately.

Fix: Use a bank account where you are the sole or primary holder for demat account linking.

Scenario 3 — Digital-only bank accounts: Some neobank variants (certain Paytm Payments Bank or FI account types) face API timeouts during Penny Drop — the broker system gets no response and marks it as failed.

Fix: Link a traditional bank account (SBI, HDFC, ICICI, Axis) for the initial verification. You can add a neobank account later after activation.

KRA Holds: Why Perfect Documents Still Get Rejected

There is an invisible layer in India’s financial system that most beginners — and most blog articles — never mention: the KYC Registration Agency (KRA). Your KYC is not only checked by your broker (Zerodha, Groww, Upstox). It is cross-checked against a central government database managed by agencies like CVL, NDML, and Karvy.

If your KRA status is “On Hold,” the broker legally cannot activate your demat account — no matter how perfect your new PAN and Aadhaar uploads are. The broker is not blocking you; the central system is.

1. Go to cvlkra.com

2. Enter your PAN number

3. Check your KYC status — if it shows “On Hold” or “Registered (not validated),” click the email/mobile validation link on the same page

4. Validate using your current email or mobile OTP

Once validated, your KRA status updates within 24–48 hours — and your broker application can proceed normally. This check takes 5 minutes and can save you days of confusion.

Myth vs Reality: What Brokers Actually Check

Several widely repeated beliefs about the demat account process are only partially true — or flat-out wrong. Here is what actually happens behind the scenes:

| Common Myth | What Actually Happens |

|---|---|

| “Income proof is always required to invest.” | Income proof is only required for Futures & Options (F&O) trading. For regular share buying, ETFs, mutual funds, and IPOs — no income proof needed. Brokers internally flag accounts for derivatives access separately. |

| “Aadhaar is optional — I can use passport instead.” | Technically true, but passport creates significant friction. Aadhaar e-KYC is the default path for all major brokers — it is faster, cheaper for the broker, and regulatorily preferred. Choosing passport means manual processing, longer wait times, and possible branch-level verification. |

| “Brokers check every document in detail.” | Initial checks are fully automated — OCR software reads your PAN, Aadhaar, and bank details; name-matching algorithms compare them; expiry dates are flagged by system rules. Only cases that fail automated checks go to a human reviewer. Submitting clean, clear documents means you never reach that queue. |

| “The process is 100% paperless for everyone.” | For individual accounts with Aadhaar-linked mobile — yes. But joint accounts often require printing and couriering a physical form booklet. If your mobile is not linked to Aadhaar, the entire e-KYC fails and you must use the offline physical workflow. Delivery Instruction Slips (DIS) for offline share transfers also require physical wet-ink signatures. |

Why Brokers Ask for These Documents

Some beginners find the document process frustrating — it can feel like unnecessary bureaucracy. But there is a clear reason behind every document request

| Document | Regulatory Purpose | Without It |

|---|---|---|

| PAN | SEBI tracks capital gains tax across all your market transactions via PAN | Tax evasion becomes possible — hence non-negotiable |

| Aadhaar | PMLA (Prevention of Money Laundering Act) requires identity verification for all financial accounts | Account cannot be KYC-verified — cannot be activated |

| Bank proof | Ensures sale proceeds go to the correct, verified account and not to a fraudulent one | No payment linkage — trading blocked |

| Income proof (F&O) | SEBI mandates brokers assess client suitability before allowing high-risk derivatives access | F&O segment locked — cash equity still accessible |

Every SEBI-registered broker follows these requirements not by choice, but by regulatory obligation. The system protects both you and the broader financial market from fraud and identity theft. To understand more about how this regulator works, read our guide on what SEBI does and how it protects investors.

Prepared vs Unprepared — The Real Difference

The gap between a smooth account opening and a 2-week delay is almost always document readiness — not the process itself.

✅ Investor A — Documents Ready

- PAN and Aadhaar name matches exactly

- Aadhaar linked to active mobile number

- Bank statement downloaded from app — clear PDF

- Passport photo taken in good lighting

- Consistent signature ready

Result: Account activated same day.

❌ Investor B — Documents Not Checked

- Middle name abbreviated on PAN — mismatch with Aadhaar

- Old mobile number on Aadhaar — OTP fails

- Uploaded a photo of cheque book in dim light

- Signed differently on two screens during KYC

- Video KYC done in a dark room — rescheduled

Result: Application held for 9 business days.

Advantages of Digital KYC and Online Account Opening

As recently as 2018, opening a demat account required visiting a broker’s office, submitting physical documents, and waiting 7–10 days. Today, the same process takes under 30 minutes from a smartphone.

| Benefit | What It Means Practically |

|---|---|

| No branch visit | Complete the entire process from your phone — including signature, video KYC, and document upload |

| DigiLocker integration | Fetch your PAN and Aadhaar directly from the government’s document locker — reduces upload errors significantly |

| Instant verification | Aadhaar OTP verification confirms identity in seconds — no manual checking required |

| Status tracking | Most brokers send real-time SMS/email updates at each stage — you always know where your application stands |

| IPO applications | Once your demat account is active, you can apply for IPOs through ASBA (blocked amount method) directly from your bank account |

Key Takeaways

- 5 documents cover 95% of investor situations: PAN, Aadhaar, bank proof, photo, signature.

- PAN is mandatory — no alternative. Link it to Aadhaar before applying.

- Aadhaar handles both identity and address — one document, two requirements done.

- Income proof is NOT required for buying regular shares, ETFs, or applying for IPOs.

- Students can open accounts with standard KYC — no income proof, no minimum balance.

- NRIs need extra documents — passport, overseas address, NRE/NRO account.

- Most rejections are preventable — name mismatch, blurry uploads, and wrong IFSC are the top 3 causes.

- Once your demat account is active, learn how to start investing step by step.

Frequently Asked Questions

Is PAN card mandatory to invest in stock market India?

Can I invest in stocks with only Aadhaar card?

Do I need income proof to buy shares in India?

Can a student open a demat account without income proof?

What documents do NRIs need to invest in Indian stock market?

What counts as bank proof for demat account India?

How long does demat account KYC verification take in India?

Is Aadhaar-PAN linking mandatory for stock market investing?

Conclusion

The documents required for demat account India are far simpler than most beginners expect. Five documents — PAN, Aadhaar, bank proof, photo, and signature — cover the vast majority of investor situations. Income proof is only needed for derivatives. NRI requirements add a few extra steps but follow the same logical pattern.

What separates a smooth, same-day account activation from a 9-day delay is not luck — it is document preparation. Check that your PAN and Aadhaar names match exactly. Ensure your Aadhaar is linked to an active mobile number. Have a clear bank statement or cancelled cheque ready in digital format.

Once your account is active, the actual investing process begins. Read our guide on how to buy your first stock in India for the exact steps from funding your account to placing your first order.